BENEFITS & BEYOND FINANCIAL

757-974-0720

Life Insurance Plans

Life insurance is a crucial component of a comprehensive financial plan. Whether you're a young professional, a family with dependents, or planning for retirement, life insurance offers peace of mind and security. You choose a life insurance company that offers a type of policy and death benefits that you want, apply, and if you are accepted the insurance company promises to provide the specified amount of money to your beneficiary (this can be a relative, loved one, or even an organization) when you die, as long as you paid the required premiums.

The coverage provided by a life insurance policy can be broad, and it typically includes the following:

Financial Security for Loved Ones

In the event of your death, the policy pays a lump sum (death benefit) to your beneficiaries, helping them cover living expenses, debts, and other financial needs.

Funeral Expenses

Life insurance can help cover the costs associated with funeral and burial or cremation services. These expenses can include funeral home fees, casket or urn costs, cemetery fees, and related costs.

Debt Repayment

The death benefit can be used to pay off outstanding debts of the insured, such as mortgages, car loans, credit card balances, and other financial obligations. This helps prevent the burden of debt from falling on surviving family members.

Income Replacement

For individuals with dependents, life insurance serves as a financial safety net by replacing the income of the deceased. This ensures that the surviving family members can maintain their standard of living and cover ongoing expenses.

Education Expenses

Life insurance proceeds can be earmarked for funding educational expenses for children or other beneficiaries. This can include college tuition, school fees, and related costs.

Estate Planning

Life insurance can be part of an overall estate planning strategy. It provides liquidity to cover estate taxes and other expenses, ensuring a smoother distribution of assets to heirs.

There are several types of life insurance, each offering unique features and benefits.

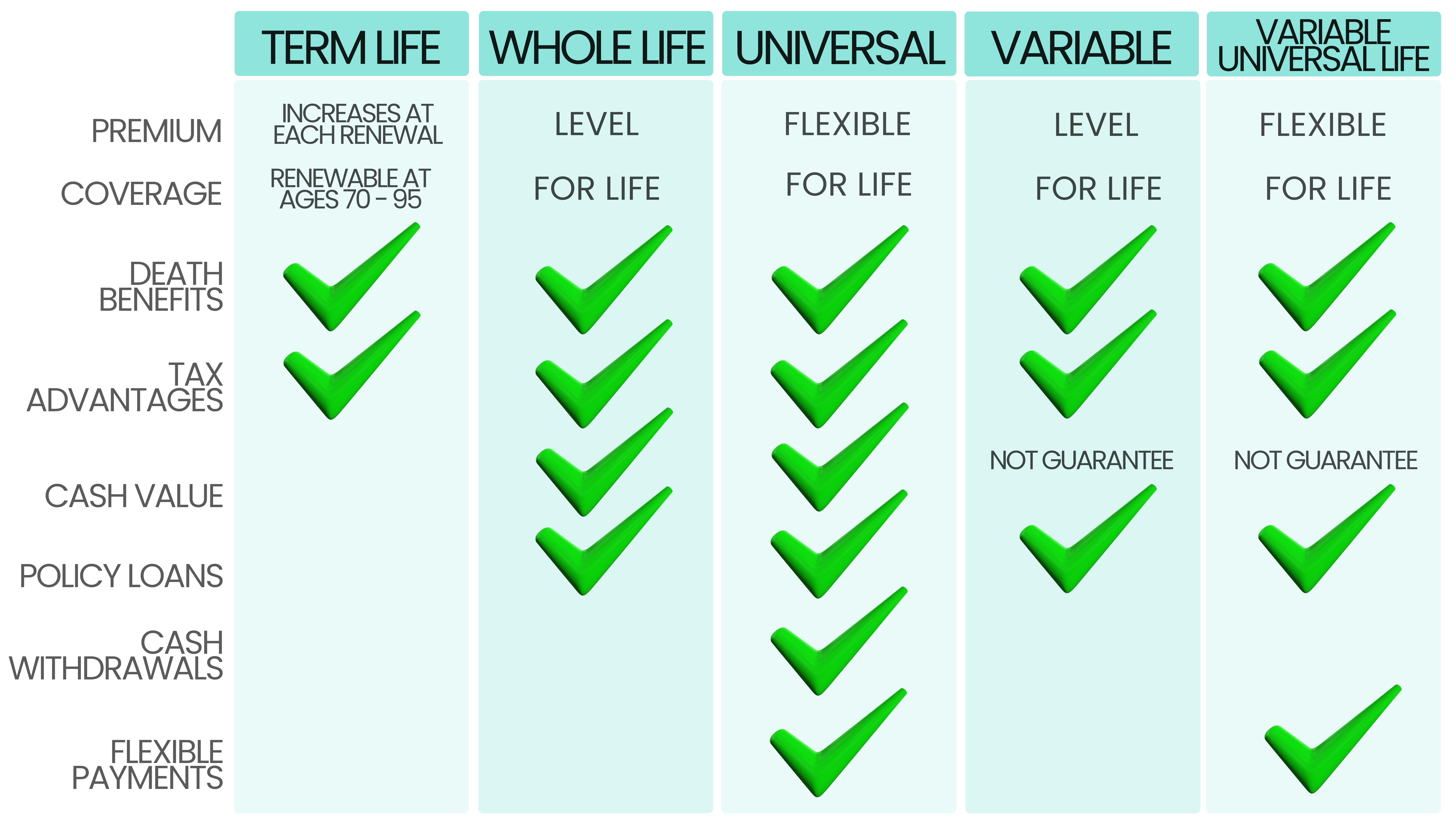

Term Life Insurance

• Provides coverage for a specific term, such as 10, 20, or 30 years.

• Pays a death benefit if the insured person dies during the term.

• Generally more affordable than permanent life insurance.

Whole Life Insurance

• Offers lifelong coverage with a fixed premium.

• Builds cash value over time, which can be borrowed against.

• Those looking for permanent coverage and cash value accumulation.

Universal Life Insurance

• A type of permanent life insurance with flexible premiums.

• Accumulates cash value that can earn interest.

• Allows adjustments to coverage and premiums.

Variable Life Insurance

• Combines life insurance with investment options.

• Policyholders can allocate cash value among different investment accounts.

• Death benefit and cash value can fluctuate based on investment performance.

Variable Universal Life Insurance

• Offers flexibility in premium payments and investment choices.

• Allows policyholders to adjust death benefits and premiums.

• The cash value is tied to the performance of investment options.

GET HELP FROM A LICENSED INSURANCE AGENT

Choosing the right type depends on individual circumstances, financial objectives, and preferences. Let one of our licensed agents guide you! Call us today or submit a request for a free consultation.

Who's This For

Parents with Young Children

Breadwinners of the Family

Stay-at-Home Parents

Homeowners with a Mortgage

Young Adults w Student Loans

Planning for Final Expenses

got a question?

Book a 15-minute meeting today!

Have questions about Medicare, health and life insurance, or retirement plans?

Let’s make it simple and clear. Schedule a quick 15-minute meeting to get the answers you need and explore the best options tailored to your needs.

Your peace of mind starts with the right information—book your session now!

Life Insurance FAQs

Who needs Life Insurance?

Life insurance provides financial support to surviving dependents or other beneficiaries after the death of an insured policyholder. Here are some examples of people who may need life insurance:

• Parents with minor children

• Parents with special-needs adult children

• Adults who own property together

• Seniors who want to leave money to adult children who provide their care

• Children or young adults who want to lock in low rates

• Stay-at-home spouses

• Married pensioners

• Families who can’t afford burial and funeral expenses

• Those with preexisting conditions

What affects your Life Insurance Premiums?

• Age (life insurance is less expensive)

• Gender (female tends to be less expensive)

• Smoking (smoking increases premiums)

• Health (poor health can raise premiums)

• Lifestyle (risky activities can increase premiums)

• Family medical history (chronic illness in relatives can raise premiums)

• Driving record (good drivers save on premiums)

What happens if I stop paying premiums?

If you stop paying premiums, your life insurance policy may lapse. Some policies have a grace period, and others may offer options like using the cash value to cover premiums temporarily.

Can I get life insurance if I have health issues?

Yes, there are life insurance options for individuals with health issues. However, coverage availability and costs may vary. Some policies may require a medical exam.

Can I have more than one life insurance policy?

Yes, it's possible to have multiple life insurance policies. People often use this strategy, known as "stacking," to tailor coverage to different financial needs.

Can I change my life insurance coverage?

Yes, you can often adjust your coverage. Some policies may allow for changes in death benefits or premiums, but it's important to check your specific policy terms.

Contact Us

(757) 974-0720

By Appointment Only

Hours: Mon–Fri 9:00am - 5:00pm

Saturday 9:00am - 2:00pm

Sunday – CLOSED

Office: 200 Kellam Rd Ste 101

Virginia Beach, VA 23462

Phone: (757) 974-0720

Fax: (757) 974-0720

COMPANY SITE

CONNECT WITH US

Privacy Policy | Terms of Use

This website represents no obligation to enroll. We are not connected with or endorsed by the United States government or the federal Medicare program. We do not offer every plan available in your area, and any information we provide is limited to those plans we do offer in your area. Please get in touch with Medicare.gov or 1-800-MEDICARE to get information on all your options.

Copyright © 2024 Benefits & Beyond Financial. All rights reserved.

Facebook

Instagram

Mail